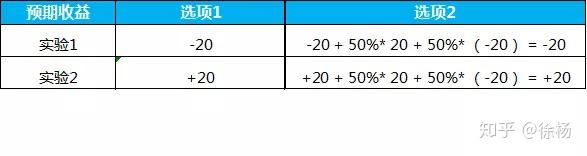

我们下面做一个小实验:

选项 1: 我们一起抛硬币,正反2面的概率都是50%。如果是正面,你能获得5000美元,反面的话,你将会损失2500美元。

选项 2 : 现在就给你1200美元。是的没错,现在就给。 你会选哪个?

根据诺贝尔奖得主Daniel Kahneman和Amos Tversky的研究结果,82%的人,会选择选项2。但是根据预期效用最大化理论,理性的投资人能够算出选项1的预期回报是$1250美元,而选项2是$1200美元。

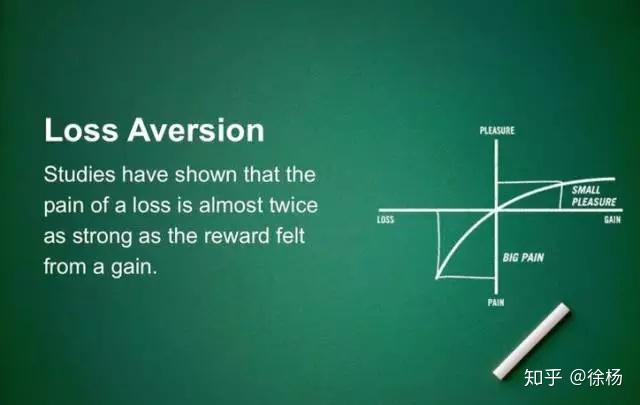

那么号称是【理性】的投资人为什么还会选择预期回报较小的选项呢? 二、展望理论 “...Choices among risky prospects exhibit several pervasive effects that are inconsistent with the basic tenets of utility theory. In particular, people underweight outcomes that are merely probably in comparison with outcomes that are obtained with certainty...” --- Daniel Kaheman and Amos Tversky "Prospect Theory: An Analysis of Decision Under Risk",1979。 总的来说,投资人在面对众多选择的时候,尽管这些选项的预期效用几乎相等, 但是投资人会更不倾向于选择确定性更低的选项。

所以对于理性的投资人,每个实验的选项都是无差别的,那么为什么投资人在不同的条件下下会有这么明显的选择偏好呢? “...The value function is normally concave for gains, commonly convex for losses, and is generally steeper for losses than for gains... which exhibits risk aversion for positive prospects and risk seeking for negative ones...” --- Daniel Kaheman and Amos Tversky "Prospect Theory: An Analysis of Decision Under Risk",1979。

发表于 2023-3-3 00:38:12

发表于 2023-3-3 00:38:12